You found the house. The roofline is right, the lot is right, the neighborhood feels right, and the inside needs work from one end to the other. For a lot of buyers in Flagstaff, that's exactly when the FHA 203(k) loan starts looking attractive. One mortgage, one path to buy and renovate, and a chance to turn a tired place into the home you want.

Then the contractor question hits.

Most homeowners assume there must be a government list somewhere with neatly pre-screened 203k approved contractors. They start searching for that list, get conflicting answers, and lose time. Meanwhile, the lender is waiting on paperwork, the seller wants movement, and the project starts to feel harder than it should.

That confusion is avoidable. The main challenge isn't finding a magical approved name. It's finding a contractor who can build well, document well, and work inside a loan process that has stricter controls than a normal remodel. If you're still trying to visualize what a neglected property could become, tools that help enhance fixer upper appeal can be useful early on, especially before you lock in scope and budget decisions.

Your Dream Fixer-Upper and the 203k Journey

A typical 203(k) situation starts with optimism and then runs straight into logistics.

A buyer finds an older home with dated finishes, worn flooring, tired windows, and a kitchen that clearly belongs to another decade. The structure may be workable, but the house isn't move-in ready in the way a lender wants. A standard mortgage may not fit the condition of the property, so the renovation loan becomes the bridge between what the house is now and what it could be.

That part makes sense on paper. The part that trips people up is execution.

Where homeowners usually get stuck

On a normal remodel, you can often choose a contractor, agree on a price, and sort out the project details directly. On a 203(k), the contractor isn't just doing the physical work. That contractor is stepping into a process with lender review, documentation requirements, scope controls, and staged payment.

If the contractor is disorganized, slow with paperwork, or casual about bids, the entire file can stall.

Practical rule: The best contractor for a retail kitchen remodel isn't automatically the best contractor for a 203(k) project.

I've seen homeowners focus on finishes first and process second. They spend their energy talking about cabinets, tile, and paint colors before they confirm whether the contractor can produce the kind of bid and supporting documents the lender needs. That's backwards. In a 203(k), paperwork quality affects whether the job even gets off the ground.

What a workable 203(k) path looks like

The projects that move more smoothly usually share the same traits:

- The scope is defined early. Homeowners know what must be repaired and what can wait.

- The contractor understands controlled payment. They aren't expecting a loose, retail-style deposit and handshake arrangement.

- The lender and consultant get complete documents. Missing details create drag.

- The homeowner stays realistic. A fixer-upper with financing oversight won't behave like a simple weekend remodel.

That last point matters in Flagstaff. Mountain weather, older housing stock, and local contractor availability can already complicate a standard renovation. Add FHA-style administration and you need a builder who can handle both field conditions and file conditions.

The contractor is the hinge point

The home may have potential. The loan may be a strong fit. But the contractor often determines whether the deal feels manageable or miserable.

A good one keeps the bid detailed, answers lender questions quickly, follows the approved scope, and treats inspections as part of the job instead of an annoyance. A poor fit fights the process, misses paperwork, and turns every draw into friction.

That's why the phrase 203k approved contractors needs a closer look. Most borrowers are using it loosely. Its actual meaning is narrower, and understanding that changes how you search from day one.

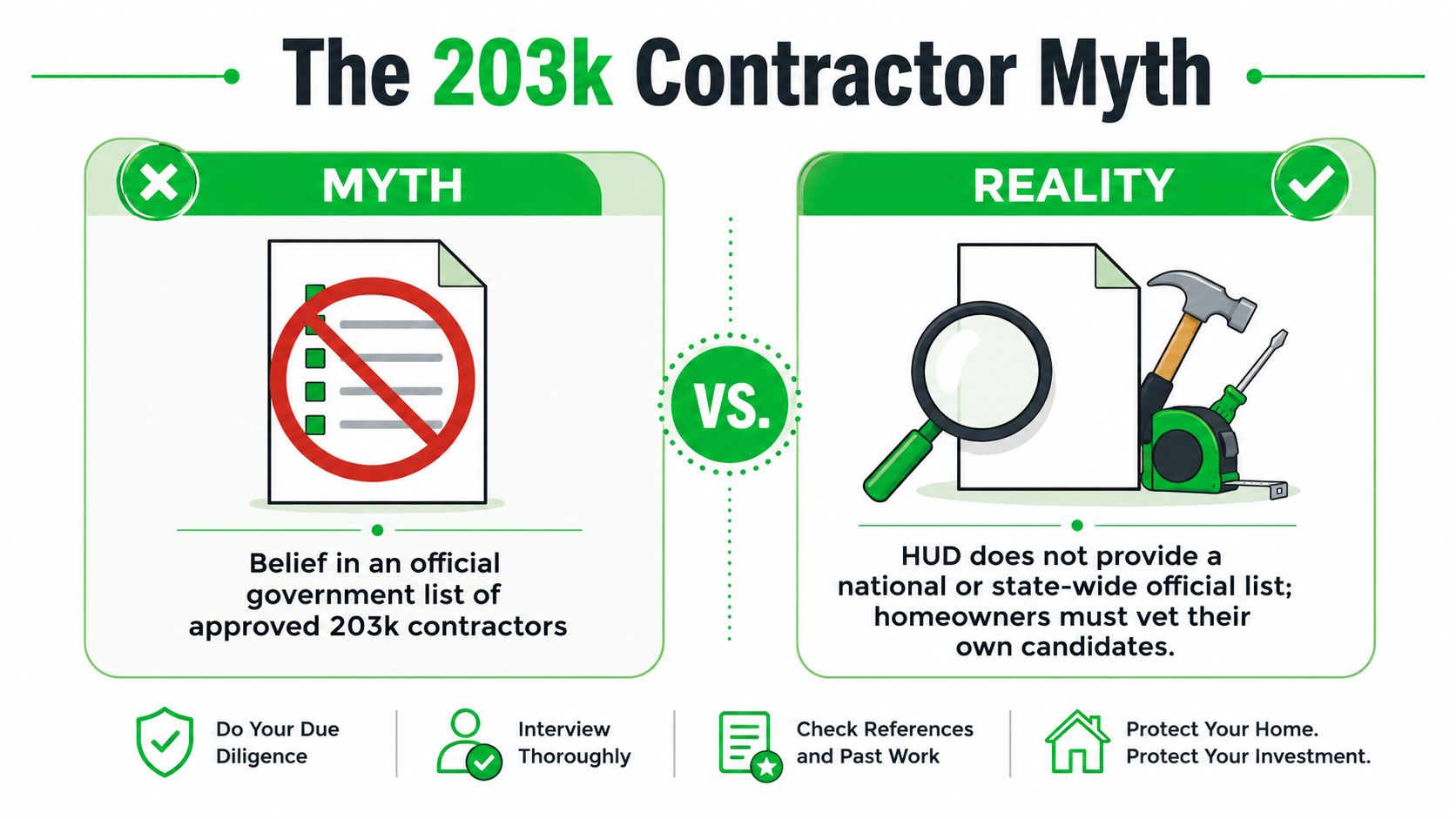

The Myth of the Official 203k Approved Contractor List

The biggest misunderstanding in this space is simple. There is no official FHA or HUD approved contractor list for borrowers to pull from. HUD doesn't certify contractors for 203(k) work. Instead, the lender validates the contractor based on licensing, insurance, bids, references, and project documentation, which makes the process contractor-agnostic but lender-controlled, as described in this contractor guidance on the 203(k) approval process.

What "approved" actually means

When people say they need a 203k approved contractor, what they usually mean is this: they need a contractor their lender will accept for that specific loan file.

That distinction matters because it changes who controls the decision.

It isn't HUD handing out a national badge. It's your lender reviewing whether that contractor is acceptable for your project. One lender may ask for a tighter package. Another may have a smoother process. Either way, the contractor still has to satisfy the lender's requirements.

Why this misconception causes problems

Borrowers lose time when they search for a list that doesn't exist. They may also trust marketing language too quickly. A contractor can say they "do 203(k) jobs," but that doesn't tell you whether they submit complete bids, carry the right documentation, or respond quickly when underwriting asks for clarification.

Here's the cleaner way to understand it:

| Term homeowners use | What it usually means in practice |

|---|---|

| 203k approved contractor | A contractor the lender accepts for the file |

| HUD approved contractor | Usually inaccurate wording |

| Certified 203(k) contractor | Marketing language, not official FHA certification for borrowers |

Borrowers don't need a government-issued contractor designation. They need a contractor their lender can vet and live with.

What the lender is really evaluating

Most lender review comes down to practical credibility and compliance:

- Licensing status so the builder is operating legally where required

- Insurance coverage because the lender wants the job insulated from obvious risk

- Bid quality so the scope and price can be reviewed clearly

- References and project documentation so the lender can assess whether this contractor is workable

That's why a solid local contractor with no flashy "203(k) branding" may still be a better choice than someone who markets heavily but can't get documents in on time.

Where to Find Qualified 203k Contractor Candidates

Once you stop looking for a government list, the search becomes more productive. You're not hunting for a label. You're building a shortlist of contractors who can survive lender review and perform under a controlled renovation process.

Start with the lender

Your lender is often the fastest place to get useful names. Not because the lender has an official FHA list, but because loan officers and processing teams often know which contractors have already made it through their documentation standards without unnecessary drama.

Ask a direct question: which contractors have previously submitted complete renovation packages and moved through the process without constant corrections?

That question is better than asking for "approved contractors." It gets you closer to what matters, which is operational fit.

Ask the 203(k) consultant for referrals

The FHA 203(k) program includes a formal consultant roster managed by HUD. Consultants must meet defined qualification paths, such as being a state-licensed architect or having 3+ years of experience as a general contractor, and they must be recertified every 2 years, which gives the process a structured framework, as outlined in HUD roster guidance referenced here.

A good consultant usually knows which contractors understand work write-ups, inspections, draw requests, and revisions. That network can save you from interviewing builders who are perfectly competent in the field but poor fits for this financing structure.

Use local industry connections carefully

Local building associations, supplier counters, and trade contacts can still help. They just need to be filtered correctly.

A contractor with a strong local reputation may be excellent, but you still need to ask whether they can function inside a lender-controlled rehab file. In other words, local credibility gets them onto your candidate list. It doesn't finish the vetting.

Consider the strengths and limits of each source:

- Lender referrals: Best for paperwork fit. Sometimes limited to a smaller circle.

- Consultant recommendations: Strong for process awareness and draw-stage coordination.

- Local trade networks: Good for field reputation, schedule reality, and workmanship history.

The best shortlist is mixed

Don't build your list from only one source. A lender referral may be organized but booked out. A consultant referral may know the process but not your exact type of renovation. A local contractor may have strong crews and weak admin support.

Mixing sources gives you better comparisons.

The strongest candidate usually isn't the person who talks the most about 203(k). It's the one who can answer scope questions clearly, produce a clean bid, and act like documentation is part of the job rather than an attack on their time.

How to Vet a Contractor for Your 203k Project

A contractor can be honest, skilled, and still be the wrong fit for this kind of loan. That's the hard truth homeowners need to hear.

203(k) work asks for more than craftsmanship. It asks for organization, patience, and the ability to keep moving when paperwork, inspections, and lender requests start slowing the rhythm of a normal remodel.

Check the documents before you discuss design dreams

Start with the basics. Before you get drawn into material selections or timeline promises, verify that the contractor can provide the documents your lender will expect. If they hesitate here, that matters.

Look for:

- Current license information where state or local rules require it

- Liability insurance documents that are current and readable

- Workers' compensation information if applicable to their operation

- A detailed written bid that matches the actual scope being discussed

If the bid is vague, the project is vague. And vague projects don't work well in a controlled loan environment.

Ask questions that expose process maturity

A homeowner doesn't need to interrogate a contractor like an auditor. But you do need questions that reveal how they operate when the job gets procedural.

What happens if the lender or consultant asks you to revise the bid?

How do you handle draw request paperwork?

What do you do when a change in scope comes up after work starts?

Have you worked on projects where inspection approval affected payment timing?

Those questions tell you more than "How long have you been in business?"

For broader guidance on hiring a reliable contractor, it's worth comparing general contractor best practices against the added demands of a renovation loan. The overlap is real, but 203(k) projects require more administrative discipline.

Use the jobsite test and the desk test

A contractor for this kind of work has to pass two tests.

The first is the jobsite test. Can they build? Do they communicate clearly about sequence, trades, materials, and likely problem areas?

The second is the desk test. Can they produce clean paperwork, answer email, revise scope notes, and keep records straight enough for lender review?

Many homeowners focus only on the first test. That's a mistake.

If you're evaluating the condition of the home itself before renovation details firm up, services tied to residential exterior cleaning in Flagstaff can also help owners see window condition, dust buildup, and deferred maintenance more clearly before final scope decisions are locked in.

A useful way to separate candidates is to watch how they respond after the meeting. The organized contractor usually sends follow-up information promptly and in one package. The chaotic contractor sends scattered texts, partial numbers, and verbal assurances.

Here's a quick reality check. Not every licensed contractor wants this work. The paperwork, inspections, and draw request process can increase administrative burden and slow payment, which is why the primary challenge is finding someone willing and able to perform under the program's documentation constraints, as discussed in this overview of 203(k) contractor requirements.

Red flags worth taking seriously

Some warning signs aren't subtle:

- They push for a quick signature. That often means they don't want scrutiny.

- They resist detailed paperwork. On a 203(k), resistance here becomes your problem later.

- They dismiss the consultant or lender process. That attitude usually turns into delays.

- They promise easy changes later. Change is possible, but never as casually as they make it sound.

- They can't explain payment flow. If they don't understand staged payment, expect friction.

A short video can help reinforce what good screening looks like in practice.

A strong 203(k) contractor doesn't just build the project. They keep the file healthy while the project is being built.

Navigating Timelines, Payments, and Project Changes

Once the lender accepts the contractor, many homeowners think the hard part is over. In reality, discipline matters most at this point.

A full 203(k) project usually doesn't pay the contractor like a standard remodel. Contractors are typically paid in up to five draws, the work generally must be completed within six months of closing, and a contingency reserve of 10% to 20% is standard for unforeseen issues, according to this FHA 203(k) loan overview.

Why the draw system changes contractor behavior

The draw system is designed to control risk. Money is released as work is completed and inspected, not merely because the calendar moved forward. That protects the loan structure, but it also changes who wants the job.

A contractor has to float labor, manage ordering carefully, and stay aligned with the approved scope. If they miss a milestone or submit an incomplete draw request, payment can slow down. That's one reason some builders price these jobs cautiously or pass on them altogether.

Field note: A contractor who is excellent at cash-pay remodels can struggle badly when payment depends on inspection-backed draw requests.

The contingency reserve isn't spare money

Homeowners often misunderstand the reserve. It's not a casual fund for upgrades you think of later. It's there because renovation work tends to uncover problems once walls, floors, or structural elements are opened up.

That's why smart borrowers treat contingency as protection, not opportunity.

A good habit is to separate three ideas in your mind:

| Budget item | What it does |

|---|---|

| Base scope | Covers the planned renovation work |

| Contingency reserve | Covers legitimate surprises discovered during the project |

| Wish-list upgrades | Often need separate review and may not fit the approved scope |

If you're still organizing project costs at the planning stage, guidance on planning your home renovation budget can help homeowners think more clearly about priorities before the scope gets locked.

Delays usually start small

Most 203(k) timeline problems don't begin as disasters. They start as small misses. An incomplete scope. A late material choice. A contractor who took on too many jobs. A change request that wasn't documented cleanly.

On renovation projects, cleanup timing matters too. Dust, debris, and residue can interfere with final presentation and punch-list clarity, which is why homeowners often schedule post-renovation dust and debris cleaning near the end of the project rather than treating cleanup as an afterthought.

When a project starts drifting, the remedy is usually not more optimism. It's tighter communication, cleaner paperwork, and faster decision-making from the homeowner. A 203(k) rewards borrowers who stay engaged.

The Final Step Putting the Shine on Your New Home

By the end of a renovation, most owners are focused on the big wins. The new kitchen works. The flooring is in. The paint is dry. The house finally looks like the place they imagined when they first walked through it.

Then sunlight hits the glass.

Construction leaves a very specific mess behind. Fine drywall dust settles where you don't expect it. Paint overspray and adhesive residue cling to windows. Screens collect debris during the work. Even a well-managed project can look unfinished if the cleanup isn't handled with the same care as the build.

Often, homeowners make one last mistake. They treat post-construction window cleaning like regular house cleaning. It isn't. Freshly renovated homes need careful detail work, the right tools, and technicians who understand how to remove residue without damaging glass, frames, or screens.

Why the final cleanup deserves professional handling

Professional post-construction cleaning isn't about making the house merely look better. It's about seeing the results clearly and protecting what was just installed.

A proper finish on the window side means more than a quick wipe. It means screen removal, screen cleaning, careful glass cleaning, and screen reinstallation. It means using professional tools such as squeegees, poles, ladders, and pure-water brushes where appropriate, not improvised household methods that can leave a poor finish or create scratches.

Renovation isn't finished when the contractor leaves. It's finished when the home is clean enough to see the workmanship properly.

A local detail that matters in Flagstaff

Flagstaff homes and cabins deal with a mix of construction dust, seasonal conditions, and mountain light that makes every streak visible. That's why the finishing step matters so much here. On a remodel, clean windows change how the entire result feels.

For homeowners who want that last phase handled by a local specialist, post-construction cleaning services in Flagstaff can take care of the residue, dust, screens, and final glass detail that a standard cleaning crew often misses.

Pine Country Window Cleaning has been serving Flagstaff since 1999. It was founded by Flagstaff native David Kaminski, and it has grown into Flagstaff's largest window cleaning company. The company removes screens, cleans screens, and reinstalls them with every service, and the work is done with professional window-cleaning tools designed to care for the glass and the home.

If your 203(k) renovation is wrapping up and you want the final result to look finished, Pine Country Window Cleaning can help. Their team handles post-construction window cleaning with the professional tools, careful screen handling, and home-respectful service that renovated properties need.